Lease or Buy Equipment: What Should You Do?

Written by Mindaugas on July 22, 2019

Should your business lease or buy equipment? That is a very common dilemma many entrepreneurs encounter. What’s even worse is that there is no definitive answer to this question.

Both leasing and outright purchasing equipment come with their own positives as well as drawbacks. Making the right decision that will have a long-lasting effect on your business stems from gathering the right information and understanding alternatives.

Try our online invoicing software for free

Accept online payments with ease

Keep track of who's paid you

Start sending invoices

As each business is unique, the equipment necessary to function will differ. Investment in your equipment acquisition may range from a few hundred to perhaps thousands or tens of thousands of dollars; you need to make this investment count.

I want your business to prosper and this can only be done with the right fiscal decisions. So should you lease or buy equipment for your business? I can’t tell you what to do, but I can help guide you. Knowledge and information within this post will allow you to come up with a proper resolution that benefits your business today and tomorrow.

Benefits of leasing equipment

To start things off, I will go over some universal benefits that leasing equipment can offer. The benefits are not industry specific, so regardless of the business you operate, you can reap these leasing rewards.

Stay up-to-date

Technology evolves so rapidly, that it is often impossible to keep up with the latest and greatest. It’s great for a business to have access to all the new technology that is available, without breaking the bank.

Computers, printers, phones, and other technology become outdated rather quickly. Some manufacturers even rely on planned obsolescence to shorten the life-cycle of the equipment they produce, in hopes you go out and buy the newest model.

Leasing gives you the ability to acquire the latest technology without large up-front payments. When your lease has concluded, you’re able to move on to the next, more up-to-date piece of tech. You don’t have to worry about having this archaic asset on your hands any longer, as the leasing company just reclaims it.

New tech and digital safety

Having access to new tech – especially tech pertaining to business IT infrastructure – can safeguard your business.

Cyber-security is a hot-button issue in today’s business environment. A business that is able to acquire up-to-date tech equipment can circumvent data breaches and other costly digital calamities.

One issue arose when computers running outdated Windows XP operating system were caught up in a massive ransomware attack. Microsoft, the company behind Windows operating system has stated – “we recommends that customers upgrade to the latest version of Windows.”

Often times, to run the newest software, you need the latest hardware. If your bank account isn’t flush with cash, a lease option can still offer you some solace.

Operational safety

Aside from the digital safety, new equipment can also improve operational, on-site safety. What do I mean by this? Well, new equipment typically comes with additional safety measures that were absent before.

Let’s use the automobile as an example. Cars have evolved rather quickly in the recent years. Some now possess autonomous driving capabilities. Cars can also stop without your input in case of a road obstruction, and new alloys are being incorporated within the frame of the car to reduce any damage inflicted on the passengers in case of a collision.

Operational safety measures are incredibly important to have in large pieces of equipment, such as cars, farm and industrial machinery. With new equipment on-hand, not only are you improving productivity, but also improving the working conditions for your employees.

Price tags on cars and industrial equipment can be hefty – that’s where leasing may shine through for you.

Small initial investment

Having cash on hand may be a short-lived endeavor if you choose to purchase your equipment. Opting in to lease instead can void major dent in your cash reserves.

When you lease equipment, down payment is not necessary – if it is, it’s typically a small percentage of the overall cost. Depending on other business related expenditures, this can ease the burden on your bank account.

We could get the systems we needed without paying a large lump sum that would have stifled other areas such as marketing, which are vital to continue our growth. – Lee Murphy, founder and CEO of Pandle

You can still get your hands on the nifty gadgets your business needs, while still having money on hand to tend other matters.

Fixed monthly cost

When leasing equipment, fixed monthly payment will be required of you to cover said lease. This is a predetermined expense that won’t change, making it easier to micromanage your business accounts and anticipate future cash needs.

Stay competitive among the big players

Without forking over big bucks and with the help of leasing options, your business can become a more formidable player in the market.

There is some quality technology out there that may be financially out of reach for many smaller ventures – unless it’s being leased. In order to stay competitive, it may be in your best interest to acquire technology that would otherwise be unattainable through leasing.

Tax deductible expense

Expenses pertaining to your lease can often be deducted from your taxes, leading to an overall decrease in your lease payment. As tax laws go, they vary drastically from region to region, so look into your local regulations to see if equipment leases are subject to business deductibles.

Leasing Drawbacks

Leasing does come with it’s downsides, that may sway you to perhaps reconsider this as an option. I want to present you both sides of the coin, so let’s look at what the drawbacks of leasing are.

Interest payments

I did make a point before-hand that initial investment through leasing is comparatively smaller than buying. However, over a long period of time, leasing is subject to interest. This means that over the course of your entire lease you will end up paying more money for a piece of equipment.

Pay attention to the interest associated with the lease option and if the rates are fixed. Often times people tend to overlook these important details, and only begin noticing discrepancies once the first monthly payment is due.

You don’t actually own the equipment

Like renting an apartment, in the end of the day, leased equipment is not yours to keep. There is no way to build equity, and once the time has come, it needs to be returned.

This can become a bigger detriment for pieces of equipment that don’t depreciate or don’t become obsolete quickly.

Obligation to pay

You have signed a lease agreement – you are obligated to abide by the agreement until the terms have concluded. Even if you don’t utilize the equipment you have chosen to lease, the payments still need to be made.

If your business is dynamic, and is subject to many changes, your equipment may need to change along with the business. Depending on your lease agreement, you could be stuck bearing the burden of additional payments on equipment that is no longer necessary..

Benefits of Buying Equipment

Now let’s take a gander at the benefits that come with buying your business equipment. Again, which option seems more appealing to you will stem from the financial status as well as short and long term business goals.

It’s easy

Buying process is simple – you see something you want, and have the money on hand, you take it and go. There is less paperwork involved and you have your equipment on hand ready to be used.

Leasing on the other hand is a bit more nuanced, compared to a simple purchase. When you are looking to lease equipment, it takes time to organize paperwork and negotiate leasing terms. Companies that offer leasing options could ask you to provide financial statements, and may inquire you on how the equipment will be used in your business.

It’s yours!

Buying a piece of equipment means it’s yours for good. This is a big advantage when the equipment in question doesn’t become outdated quickly such as furniture, vehicles and farm equipment.

Some assets you purchase may not even depreciate quickly. Perhaps once the time comes to part ways with your asset, you could recoup a big portion of your initial investment back by selling the equipment.

Maintain on your own terms

Ownership allows you to maintain your property anyway you wish. When you buy equipment for your business, there are no stringent maintenance guidelines that you have to follow. Leasing equipment often comes with specific requirements which you must follow in order to stay within the confines of the agreement.

Tax incentives

Like leasing, buying equipment for business use also comes with potential tax incentives.

As I have mentioned before, taxes and business deductions operate differently based on the region or the country in which you operate. I will use United States as an example to show you possible tax deduction you can take advantage of.

In the United States, according to Section 179 of the IRS code, you can fully deduct a portion of the cost associated with new equipment purchase.

Here is how it works:

Since 2018, the deductions can also be applied to land and building acquisition.

No interest fees

Interest fees that are associated with leasing can be nasty. Not only is leasing temporary, but you end up paying more for the equipment you need in the long run.

When choosing to buy your equipment for your business operations, there is no interest fees. It’s a simple payment forgoing any future interest build-up.

Drawbacks of Buying Equipment

You have to take the good with the bad, so again buying equipment will also have some negative aspects. With this guide I intend to be impartial, so you need to be aware of everything associated in regards to acquiring equipment for your business.

A potentially large upfront payment

Depending on the type of equipment you’re looking to purchase, the sum required to complete the purchase may be too much for your business to handle. A business need to be fiscally responsible and delegate cash across variety of functions such as marketing, product developing, salaries etc. A large purchase can negatively impact other vital areas of your venture.

Being stuck with an outdated asset

Evolution in the business environment happens quickly and can often render your equipment useless. Not to mention technology itself that is being acquired can become obsolete once a new product is launched.

These variables that are out of your control can leave you with an asset that’s no longer viable. This may leave you vulnerable to competitors who do possess the latest tech on the market, improving their productivity.

Getting more than you have bargained for

I am sure you have heard of the saying “eyes are bigger than the stomach”. This can prove to be true even during the equipment purchasing process.

A business that has acquired a large client or is undertaking a major project may need a piece of technology or machinery that was once unnecessary. You choose to purchase said equipment only to realize that the necessity is short-lived. Once you have fulfilled your obligation to the client, the equipment you bought is stowed away, collecting dust.

In this regard, what you have purchased has become a situational luxury. You could end up selling it, or you may even wish to rent it out for other businesses to use.

Consider these questions before committing

When making decisions that can have a tremendous impact on your operations, you need to ask yourself some questions before moving forward. The answers you come up with may guide you to a more reasonable option that coincides with the needs and financial capabilities of your venture.

I also implore you to discuss these decisions with your employees who may be at the front-lines of equipment usage. Your associates could offer valuable information and disclose their opinions as to what may work best and which options – perhaps more affordable ones – are viable.

What lease are you going to sign?

There are two main leasing options available when looking to acquire equipment for your business.

Capital lease

A capital lease has characteristics of an asset – in regards to your balance sheet. This will have an impact on the company’s financial statements, depreciation expense, assets and liabilities.

With a capital lease, you can take advantage of tax deductibles that pertains to the asset depreciation.

Financial Accounting Standards Board (FASB) amended it’s accounting rules. Starting from Dec 15th, 2018 public companies must capitalize all leases with contract terms that are longer than one year. Private companies will have to do the same, but only starting from Dec 15th, 2019.

Operating lease

When you sign an operating lease, the company from which you lease the piece of equipment will retain its ownership. When looking at this from the accounting point-of-view, operating lease is an operating expense.

Operating leases are short-term commitments. Smaller businesses tend to utilize operating leases more often as it allows them to retain most of their cash on hand.

How long will you use the equipment?

Assess the length of time you expect to use the equipment. This will play a role in what type of lease agreement you may need to sign or if a purchasing the equipment may be more beneficial to you.

Do you have cash on hand?

If you have available cash stowed away? It could be more beneficial to outright buy your equipment rather than leasing it. This will of course go in hand with the potential expected lifetime of the equipment.

Have you considered used equipment?

Previously, I touched on the benefits that new technology and equipment can offer for your business. Fact is, this is very situational – your needs and functionality that equipment endows you with will vary.

If you run a design firm that specializes in creating 3d graphics, you probably need access to great hardware and software to keep the competitive edge. If you are an author, a used computer will suit you just fine.

Your business and its functions will dictate whether you should opt for new equipment, or if you can get away using used or refurbished equipment.

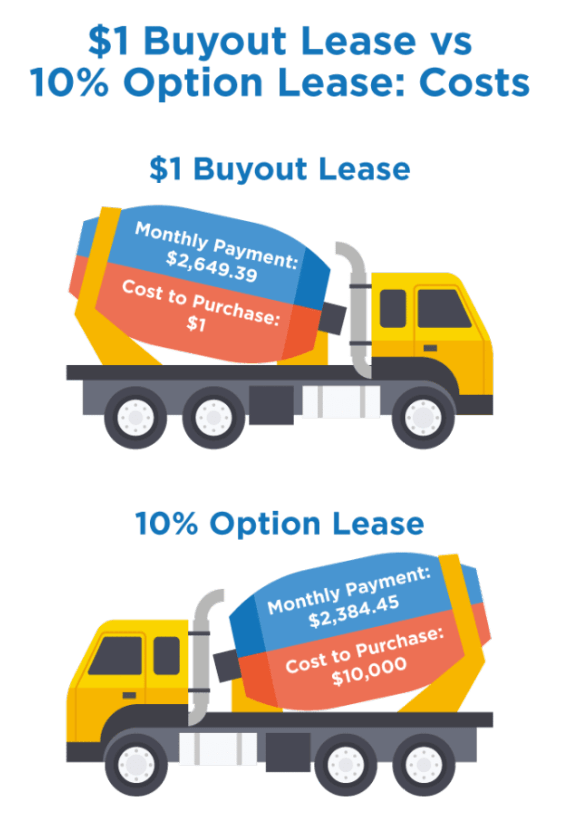

Does the lease offer buyout options?

When it comes to leasing, at the end of the lease term, you may have the ability to buyout the item in question. Sometimes you can buyout the leased item before the end of your lease term. This could be something to keep in mind, if you’re considering holding on to the equipment long-term.

Is insurance necessary?

Some equipment can be rather expensive, and might need to be insured. It would be a shame if you bought or leased new equipment only for something bad to happen once you start using it. Insurance is there to help cover any liabilities associated with faulty, damaged, or stolen equipment.

In the case of leased equipment, the leasing company may require you to insure the equipment. Of course this is an additional cost associated with acquisition and the insurance amount can fluctuate.

If you decide to buy the equipment, look at any warranties that come along with the purchase, and do inquire about any potential insurance options. This could be a necessity if the investment is large and you want to reduce the chances of running into financial issues down the road due to any unforeseen incidents.

Is lease termination an option?

A few paragraphs above, in the “leasing drawbacks” section of the post, I mentioned the obligation to pay for equipment event when you’re not using it. If a lease is signed, you could be stuck making payments for the extent of the lease…unless there is an option to terminate the agreement.

Before the pen hits the paper, and you commit to the lease, inquire the lessor about termination options – if there are any. Check and see if there are any penalties associated with termination as well. You want to minimize the risk of running into unexpected costs later on.

Time to make the choice

Choosing to either lease or buy equipment for your business can be a nerve-wrecking experience. These are the essentials that your business operations will be relying on for the foreseeable future; not to mention the need to part ways with some cash.

Anxiety can be circumvented by endowing yourself with the right information before taking this plunge. I hope that I was able to provide you with some of the valuable insights which will mitigate any doubts moving forward with your choice.

Good luck!