5 Essential Small Business Financial Trends for 2026

Written by InvoiceBerry Team on March 25, 2026

Small businesses have always operated in adaptation mode. Regulatory shifts, currency swings, another wave of digitalization promising to “simplify everything” — pick your year, the story is roughly the same. 2026 is no different, except the forces converging right now feel more structural than cyclical. Elevated interest rates across major economies, AI creeping into accounting systems, new transparency demands, and payment infrastructure finally moving toward real-time processing — these aren’t passing phases. For anyone who invoices clients, monitors cash flow, and tries not to get lost between VAT and bank charges, several things are about to change in ways that matter. Here are five worth understanding before they catch up with you.

What’s Actually Happening in the Market

Since 2024, major players (from Stripe to SAP) have been pushing financial automation tools into territory that previously belonged exclusively to enterprise budgets. Small businesses are on the receiving end of that shift now, gaining access to software that cost serious money just a few years back.

Try our online invoicing software for free

Accept online payments with ease

Keep track of who's paid you

Start sending invoices

Alongside this, outsourcing of routine financial functions has picked up considerably in B2B circles. Companies like DXC Technology — their business process services span finance automation, procurement, and HR — reflect a broader pattern: businesses offloading repetitive back-office work to concentrate on what they actually do. That logic, once reserved for larger organizations, has reached the SMB level through affordable SaaS.

A few other developments shaping the backdrop:

- Open Banking APIs — banks across the EU, UK, and increasingly North America must share account data with third parties through standardized interfaces

- AI bookkeeping assistants — tools like Intuit Assist or Xero Analytics Plus, which forecast rather than just calculate

- Embedded finance — Shopify Balance, Wix Payments, Squarespace Payments: financial services living inside the platforms people already use

- Real-time payments — FedNow in the US, Pix in Brazil, SCT Inst across the eurozone

In 2025, Puzzle.io demonstrated an expense categorization system built on GPT-4o that adapts to a specific business’s patterns within the first three months of use. Mercury, the neobank for startups, shipped a “financial copilot” that goes beyond reading transactions — it suggests when to time dividend payouts based on actual cash flow data.

Trend 1: Automation Moves from Enterprise Down to Small Business

If 2023 was when automation became a buzzword, 2025 was when actual implementation spread. In 2026, manually entering invoices into spreadsheets carries roughly the same energy as defending the fax machine.

What’s Getting Automated

The most common automation use cases for small businesses right now:

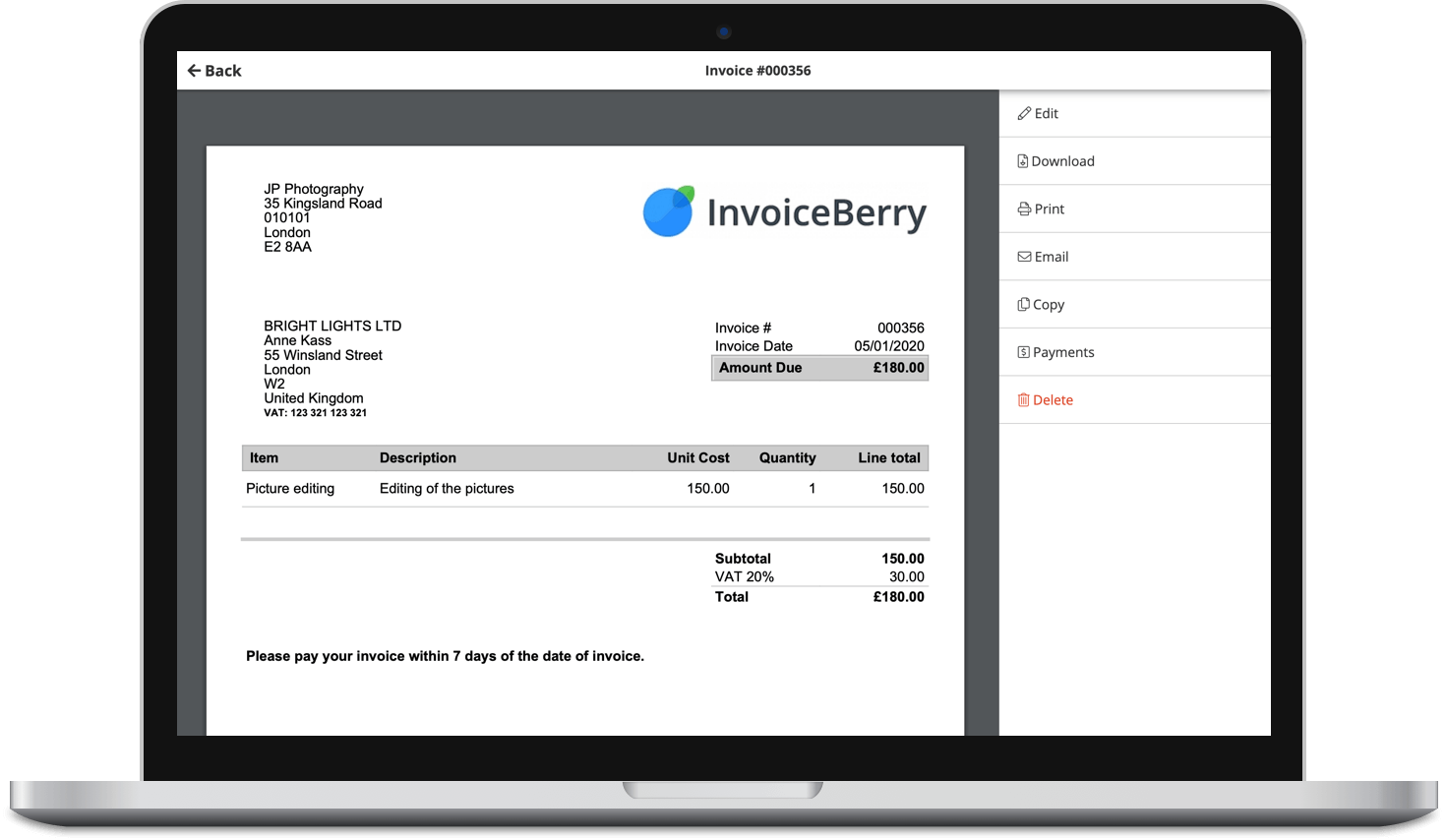

- Automatic invoicing Platforms like InvoiceBerry, Zoho Invoice, or FreshBooks generate and send invoices based on triggers: project completion, month-end, delivery confirmation

- Bank reconciliation Systems match transactions to invoices independently, without manual cross-checking

- Payment reminders. Automated follow-ups at 7, 14, and 30 days past due, no human input required

- Expense categorization. AI assigns expenses to budget lines based on vendor patterns and transaction history

The time savings are real. Research from providers like Tipalti consistently points to small businesses spending ten to fifteen hours monthly on manual financial document processing. Automation typically brings that down to two or three hours. Several working days a month redirected toward sales or actual product work — that’s the practical math.

Trend 2: Embedded Finance: The Bank Inside Your Platform

The concept is simpler than the name suggests. Financial services no longer need to live separately from the platforms where daily business happens. Shopify merchants can receive payouts, hold funds, and access capital directly from the admin panel. Wix and Squarespace have built-in payments. HoneyBook and Dubsado (project management tools for freelancers and agencies) now handle invoicing and collection natively.

What embedded finance offers:

- Fewer tool-switches between payment processor, bank, and accounting software

- Revenue and expense data in one place, without manual exports

- Often better rates, since platforms subsidize financial services to retain users

- Credit access based on actual business activity rather than traditional credit scoring, which can be especially useful for businesses working with a Shopify ecommerce agency to scale faster without relying on traditional financing barriers.

The downsides:

- Vendor lock-in becomes real when the entire financial stack lives inside one platform, even if your Shopify store can be found in ChatGPT

- Terms can change unilaterally — payout schedules, fee structures, credit limits

- Not every embedded account carries the same regulatory protections as a licensed bank deposit

Multiple fintech research firms project embedded finance will account for a significant portion of small e-commerce financial activity across North America and Europe by end of 2026. Businesses looking to stay competitive are increasingly investing in fintech software development to build secure, integrated financial experiences. As competition within the sector increases, many companies are investing in FinTech paid social strategies to improve brand visibility and customer acquisition. The direction is consistent across forecasts even where precise figures differ.

Trend 3: AI in Financial Analytics: From Dashboards to Actual Recommendations

QuickBooks, Xero, Wave — familiar names. What they do in 2026 looks quite different from two years ago. The shift has been from auto-categorization to something closer to genuine financial analysis. These AI-driven insights become even more accurate when connecting accounting software with banking, payment, and invoicing systems, giving the platform a complete picture of a business’s financial activity.

Intuit Assist, embedded across QuickBooks and TurboTax, flags potential cash crunches two to three weeks out and suggests when to delay large expenditures. The system doesn’t use generic models — it trains on each business’s own historical data. Xero Analytics Plus offers scenario modeling: “what happens to cash flow if a major client delays payment by 30 days?” For small businesses where one contract can represent half of monthly revenue, that’s a real risk management feature.

Notable AI features in financial tools for 2025–2026:

| Feature | Platform | What It Does |

| Intuit Assist | QuickBooks | Cash flow forecasting, cash crunch alerts |

| Xero Analytics Plus | Xero | Scenario modeling, receivables analysis |

| Puzzle AI Categorization | Puzzle.io | LLM-based expense categorization |

| Mercury Copilot | Mercury Bank | Transaction analysis, fund allocation suggestions |

| Stripe Sigma + AI | Stripe | Natural language queries against financial data |

AI still stumbles in a few areas worth noting: non-standard tax jurisdictions, complex multi-currency operations with hedging, and situations where context simply doesn’t exist in transaction data. No substitute yet for a human accountant who knows the full picture.

Trend 4: Real-Time Payments and Open Banking

Traditional banking with T+1 or T+2 settlement looks increasingly awkward in a world where everything else moves instantly. Real-time payment infrastructure is spreading faster than most small business owners track.

FedNow launched in the US in 2023 and adoption has grown steadily since. Brazil’s Pix processes billions of transactions monthly — more than credit cards. Across the eurozone, SCT Inst became mandatory for all eurozone banks from 2025. Germany, the Netherlands, and France have seen particularly fast uptake, with instant B2B transfers becoming standard expectation rather than a premium service tier.

What shifts for small businesses:

- Cash gaps shrink when payments clear immediately rather than in two business days

- Real-time bank transfers typically cost a fraction of card processing fees

- “Pay after delivery” models become commercially viable for more business types

Open Banking layers on top of this: standardized APIs let accounting software connect directly to a business bank account, without manually downloading statements. In the UK, this is already the baseline — Tide, Monzo Business, and Starling Bank support it natively, with dashboards that update in near-real time.

Trend 5: ESG Reporting Is Starting to Reach Small Suppliers

ESG can seem like a large-company concern. It’s becoming less so. If a small business supplies goods or services to larger companies, sustainability transparency requirements are already traveling down the supply chain.

The EU’s CSRD expanded in 2024 to cover large companies, and those companies are now requesting ESG data from their suppliers — including small ones. Several procurement teams at major European retailers and manufacturers have already added sustainability questionnaires to standard supplier onboarding processes.

What to Start Tracking

Minimum useful metrics:

- Energy consumption in the office or production space (kWh per month)

- Share of cashless transactions — less physical cash means a smaller footprint from cash-in-transit logistics

- Waste generation and disposal method

- Gender balance and pay equity indicators within the team

Tools for smaller businesses:

- Greenly: calculates carbon footprint automatically from bank transaction data

- Watershed: more comprehensive, with pricing tiers for companies under 50 people

- Cozero: built for small manufacturing operations

ESG isn’t only a compliance cost. Businesses with documented sustainability practices are gaining access to green credit lines at lower rates — banks in several EU countries and Canada already offer rate reductions for businesses that can verify specific ESG metrics. The financial upside is becoming harder to dismiss.

Practical Checklist for 2026

- Check whether your accounting system supports Open Banking API in your country

- Audit how many hours per month go to manual invoice and statement work — identify what’s actually automatable

- Ask your bank whether they support real-time payments and what fees apply

- If large corporate clients are based in the EU, find out whether they’re already requesting ESG data from suppliers

- Review embedded finance options in platforms you already use — the terms are sometimes better than current bank arrangements

Conclusion

These five trends aren’t separate threads — they reflect the same underlying movement: finance getting faster, more automated, and harder to ignore. Small businesses that treat these changes as background noise tend to find themselves adjusting reactively, at worse timing. Engaging with even one or two of these areas now (whether that’s connecting accounting software to Open Banking or reviewing embedded finance options) tends to compound over time. The gap between early adoption and playing catch-up widens quickly in financial infrastructure.

Small Business Finance 101

Download our free guide to learn the fundamentals of finance that will help make your small business more efficient and successful.