Wouldn’t it be easier if you could predict, at least partially, the success of your business?

Well, that’s possible as long as you know and track a few essential financial numbers. If you don’t track your finances, you’ll take on too much debt, and this will obviously set you up for failure in the long term.

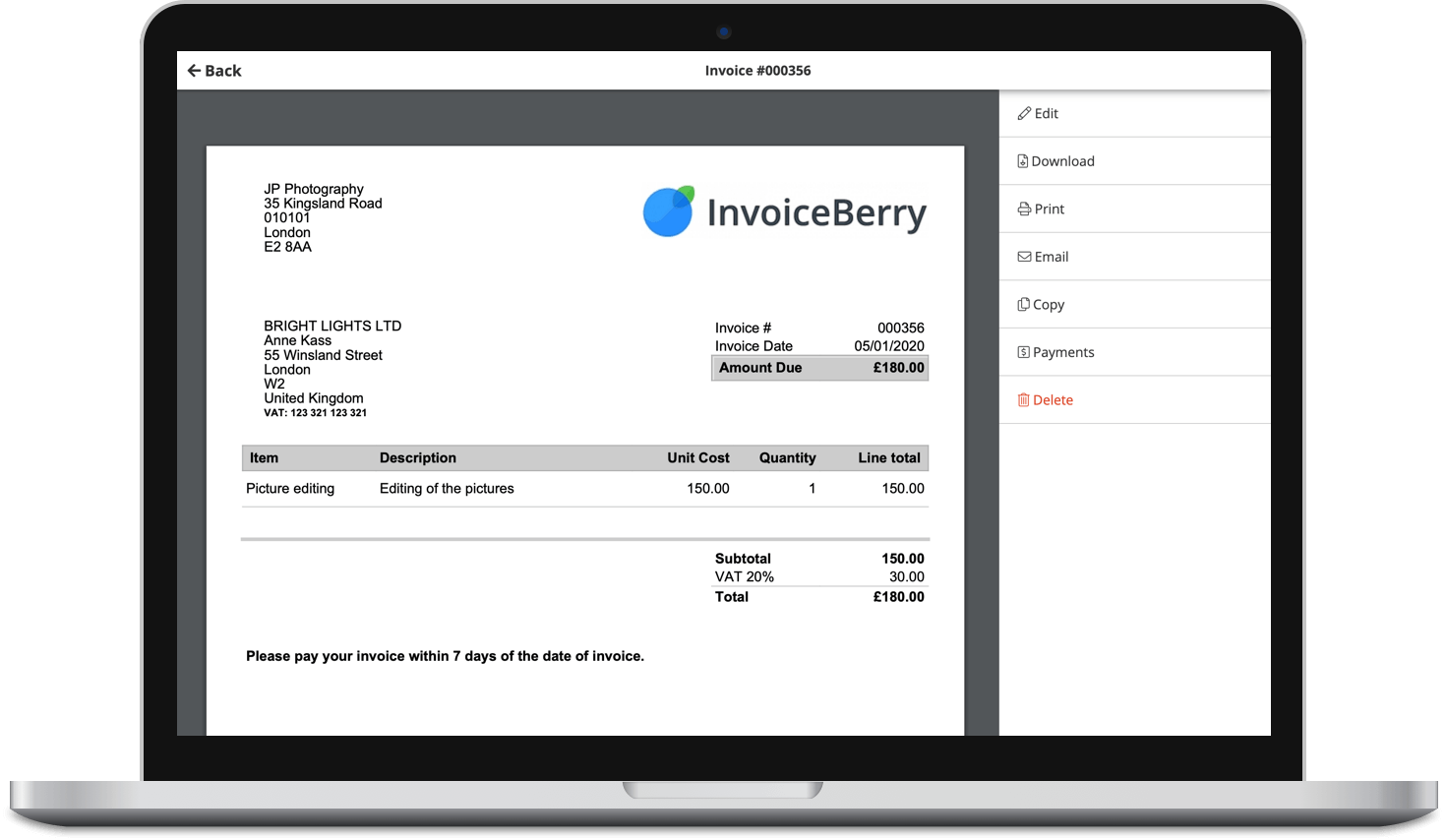

Try our online invoicing software for free

Accept online payments with ease

Keep track of who's paid you

Start sending invoices

You need to monitor your cash flow, net income, profit and loss, sales and gross margin, as well as your total inventory to ensure that you won’t be facing any potential issues in the future.

Here are 5 critical numbers every small business owner should know and track.

1. Cash Flow

Cash flow is essentially the amount of money you get by subtracting operating expenses from the money your company generates during normal business activities.

Sufficient cash flow in your business checking accounts is essential, and should meet all of your business’ monthly expenses.

When your cash inflow exceeds your cash outflow, it means you’re operating “in black” — in essence, your return on investment is higher (and so is your profit).

Download cash flow template right here.

2. Net Income

Want to know if you’re losing money? Calculating your net income is the easiest way to find out.

To do is, simply subtracting all your expenses, including taxes, from your income. Unlike cash flow, your net income isn’t adjusted for things like depreciation.

To know just where your business is heading to, make sure to calculate your net income every month.

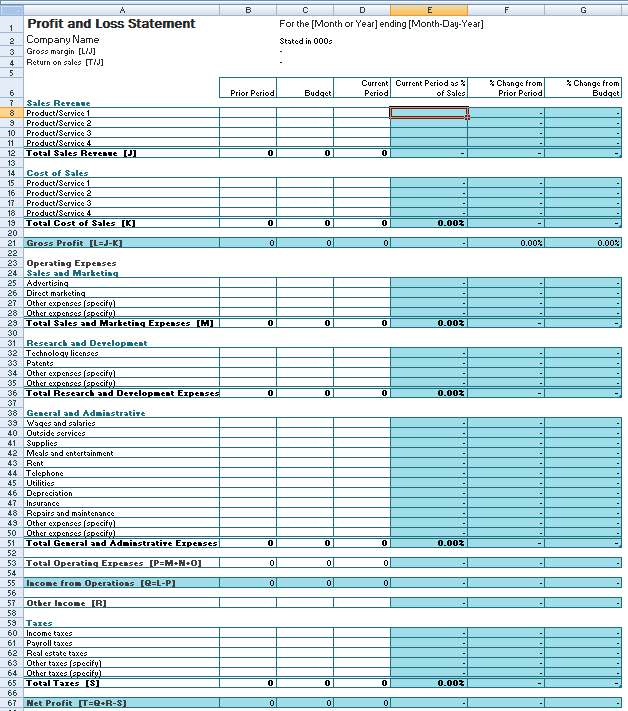

3. Profit and Loss

Making realistic plans for the future, both short term and long term, is absolutely critical to the success of your company.

Many companies set goals but due to the lack of a strategic business plan, they end up taking on more debt.

Profit and loss is a figure found on your P&L statement, and shows your company’s income (sales and revenue) minus expenses during a certain period of time (quarterly, every six months, or yearly).

If you want to predict the success of your small business, always explore your profit and loss to project earnings, and allow your company to grow gradually.

Download free profit and loss template from here!

4. Sales

Generating sales (and revenue) is every small business owner’s primary objective. Keep an eye on sales to monitor when there’s a dip and when business is good, so you can adequately react and take action.

5. Gross Margin

When we say gross margin, we refer to the amount of money that is left after subtracting the cost of the merchandise from the selling price (e.g. if you’re buying, say, a laptop for $300, and you’re selling it for $700, then your gross margin will be $400).

If your gross margin is low and doesn’t cover your business monthly expenses such as salaries, utilities and marketing, then you’re not charging enough for your products.

![]()

Always Keep Track of Your Finances

The number-one mistake that leads small businesses to failure is not keeping track of finances. Instead of spending hours going through invoices and reports, let InvoiceBerry do the job for you!