As an SMB, your finances are all you’ve got. If you ever want to scale up and thrive as a business, you should make sure your finances are in check. But, with that said, finances have always been a topic shrouded by myths and misconceptions in the startup world.

Admittedly, finance can be a somewhat complicated subject for entrepreneurs since there are so many things you need to keep in mind.

Try our online invoicing software for free

Accept online payments with ease

Keep track of who's paid you

Start sending invoices

But on the bright side, there are just as many online free resources available to guide you through the journey. And even if you don’t even know the difference between your balance sheet and your cash flow statement, don’t worry – there is hope just yet.

So, in this guide, we’ll be clearing up some of the myths that surround the finance sector of the SMB world. If you’ve ever fallen for the common misconceptions that hold many entrepreneurs back, be sure to read on as we’ll be shedding light on some of those myths.

Myth 1: You don’t need a business plan

This is somewhat of a recent trend that says startups don’t need a business plan and will be fine if they just dive headfirst into the real world.

While you might survive for a year or two at most, it’s safe to say that you won’t make it far without an effective business plan. Business plans are an essential part of your long-term strategy, which includes the goals and the means through which you achieve them.

Not to mention, if you ever want to scale up as a business, you need a reference document to look back on and share with other people.

Myth 2: You won’t be able to profit for a very long time as a startup

This is another common myth that often holds entrepreneurs back.

Though, let’s first take a step back to examine the importance of profit as an SMB.

You need profit and money to survive, yes, however, if you’re just after the gross profit – you might not get far in the first place.

Instead, you should be focusing on fulfilling a certain need.

If you truly believe in your vision, you won’t gain burnout from your startup.

Though, with that said, it’s certainly possible to start making money as a startup within the year – depending on your niche and expertise. By focusing on your vision, however, you’re more likely to last longer as a business.

Myth 3: You should be prioritizing revenue over profit or vice-versa

First off – what’s the difference:

Revenue is the money you earn from the sale of goods or services and it measures the total income from sales.

Profit, meanwhile, is what you get once you subtract the expenses that go into the making of the product.

Ideally, as a startup, you should be focusing on growth and the revenue and the profit will come in naturally.

If you want to survive as a business though, you should at least have a positive level of cash flow, so, start there.

Myth 4: You must raise money up front to succeed

Of course, the more money you have beforehand – the better.

But this is not to say you won’t survive without it.

If you start things off right and start saving unnecessary expenses straightaway, you can save money and go far in your niche.

Bootstrapping is a great way to minimize costs and get to know your priorities.

With a shoestring budget, you’ll learn the importance of priorities and that you don’t need as many things as you think you do. Many companies started out this way, working from their garage and getting a loan from friends and family instead of the bank.

Myth 5: You need a lot of money to scale up and grow as a new business

This is another common myth. Of course, money is essential to growth, but not as much as you might think.

While you can save money with bootstrapping, what you can also do is borrow instead of paying, rent instead of buying and so on – you get the point.

The idea is to turn fixed costs into variable costs. This way you’ll save money that you can put into scaling up instead.

Myth 6: Banks don’t lend money to startups

According to the Biz2Credit Small Business Lending Index, big banks approved 23% of funding requests in March. While this number may not seem high, it’s still better than the alternative sources of debt (family, friends, venture capitalists, etc).

Also, this marks a trend in the loans taken from the bank for startups as it is an increase up to two-tenths of a percent from February 2016.

Your mileage may vary and it also depends on where you’re from. (For example, you have a lot of choice if you’re from the U.S.) but for the most part, the more prepared you are when going to the bank for a loan – the better.

Speaking of…

Myth 7: Venture capitalists are the only source of funding

While VCs can help you go from a 0 to a 100 quickly, they’re not the only way you can scale up.

Other popular methods include crowdfunding, kickstarters, microloans from the bank, and more.

As an SMB, you need to take a step back and ask yourself a couple of questions in regards to where you’re headed and how you’re going to get there before you advance.

Myth 8: If you build it, they will come

Let’s say you have an amazing product or a service with a lot of potential. Naturally, customers and interested venture capitalists should start flocking to you, right?

Well, this is also not the case because it’s not all about the product.

You also need to spend some time on marketing and selling the product, which are just as important for growth. And you should also be actively looking for an investor or a business accelerator.

And when scaling up, remember not to focus only on the product (by hiring more developers, etc.). Customer support and building close relations with your users are just as important.

Myth 9: If you’re unsure about your pricing strategy, just undercut your competitors

Pricing is always a complicated area as a business. And though undercutting your competitors is a common tactic – it’s not the best one.

If anything, it could lead to devaluation of your product and not even being able to break even.

So, what’s the solution here?

To ensure competitiveness and profitability of your product, you need to know it inside out (including the 4Ps: product, pricing, promotion, place), research the product and service costs involved, and finally – the customer demand.

If you’re in the SaaS (software as a service) niche, you can look into using the freemium/versioning model and see how that will work for you.

Myth 10: If you need finance, you have to sacrifice equity

Equity, or stockholders’ equity, shows up in your balance sheet and is essentially the amount of capital invested by the shareholders.

But as mentioned above, you can get far as a startup without having to lose a lot of equity through a variety of different methods.

Though banks often see startups as a risky investment, there are many other ways you can finance your business with a more flexible source of funding.

Myth 11: You’re going to be rich and live glamorously

Well… I don’t want to discourage you from pursuing your dreams but most (9 out of 10) startups fail.

Of course, there are a lot of reasons behind this (business incompetence, lack of experience, etc.) but the main point is this: if it fails, it might be because of you.

It’s often the owners who end up making the wrong business moves and go down a slippery slope.

On the bright side, failure is the best teacher.

Most startups fail, yes, but this doesn’t mean you can’t start another business venture later. And success doesn’t happen overnight.

If you’re passionate about your vision, you should definitely pursue it.

Though money is a side product and even though things can get rough, as long as you’re following your dream – then you’re already on the right track.

Conclusion

All in all, the startup world is not easy. And it’s not for everyone.

But at the end of the day, life, (like startups), is all about taking risks.

And if it doesn’t work out, you’ll come out with much more knowledge out of it than before.

Be warned though, you might not know what you’re getting yourself into. So, it’s best to familiarize yourself with some common myths and misconceptions first.

And if you’re just starting out, be sure to stay on top of your finances if you want to survive. This way you won’t get lost halfway through.

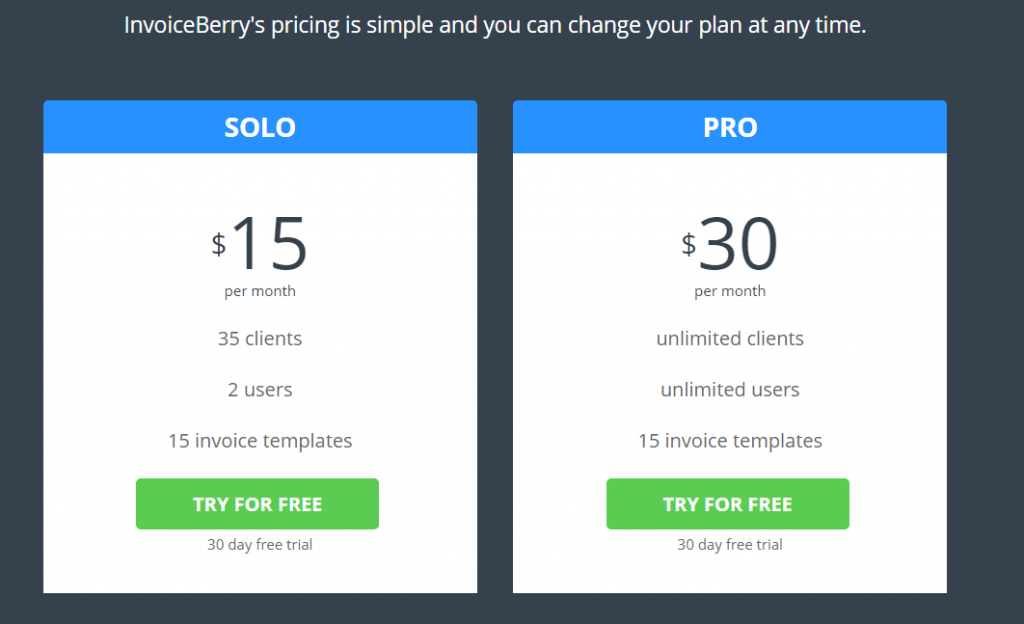

If you’re not sure how to do that, consider using online invoicing software as a cost-effective way of tracking and analyzing the financial situation of your business.