A lot of details need to be ironed out during the inception of a new business. The idea that evolves into a business is pivotal, but legal matters will require attention too. Legal structure of a business will dictate accounting processes, how personal liabilities are handled in case of lawsuits or insolvency, and the amount of paperwork you’ll be faced with.

If you’re reading this, you probably have started a business as a sole trader. Running every aspect of your venture independently invokes a sense of serenity and there are less hurdles to burden yourself with. However, making the switch from a sole trader to a limited company does come with it’s own benefits – albeit it’s a bit more nuanced.

Try our online invoicing software for free

Accept online payments with ease

Keep track of who's paid you

Start sending invoices

What’s the difference between ‘sole trader’ and a ‘limited company’?

Sole Trader

As a sole trader, the income generated from economic activity is your own personal income – and it’s taxed as such. Legally speaking, you’re the business and there are no barriers separating you as an individual from your company.

Any losses incurred are your own personal responsibility and so are any liabilities you may have. Being a sole trader, there is no need to have a business name, as you’re able to operate under your own personal legal name.

Some responsibilities as a sole trader include keeping financial records of sales and expenses, and the need to file a self assessment tax-return every year. You will also need to register for VAT if your annual turnover is over £85.000.

Limited Company

A limited company comes with variety of differences. First and foremost, a limited company operates as it’s own separate entity. Any revenue generated belongs to the company and is subject to corporation tax. Salaries, including your own, will be paid by the company.

Information will need be submitted to HMRC (HM Revenue and Customs) containing the following – annual financial records, filings with Companies House, your own Self Assessment, company’s tax return, and corporation tax.

Shareholders are also part of the equation, although you could remain the sole shareholder. You have the option to appoint yourself as the director of the company once you have decided to create the limited company.

Additional benefits of a limited company

Limited companies are subject to more tax relief than a sole trader. A limited company for example, can pay for business related outings – whether it’s a restaurant, or various networking events – it would be regarded as a business expense. Sole traders have less leeway in this regard – a tax relief can only be claimed under more stringent circumstances (e.g. a trip with an overnight stay).

Something worth considering

As a proprietor of a limited company, you no longer have free reign over your company’s bank account – the cash within the account is strictly regulated. The company pays your salary, covers dividends on the shares you or someone else own, and can reimburse business related expenses. Money used for any other purpose can be subject to additional tax.

Another thing to take note is the legal responsibility to safeguard company’s assets as a director. You are also obligated to cease trading shares if there is a chance of your company becoming insolvent. Failure to do so can bring forth severe legal consequences such as fines and in some cases a prison sentence.

A limited company is entitled to less privacy than a sole trader. When you file company’s accounts and annual return, these documents will become public information. Anyone who wishes to look your company up will have access to financial reports as well as the address of your limited company.

Deciding when to change from a sole trader to a limited company

The difficult part comes when a decision needs to be made to change from a sole trader to a limited company. It may not always be clear when a legal restructuring needs to take place – usually people consider this step when revenue begins exceeding the 30-50k range. Variables such as the industry in which you operate, and future expectations will also dictate when this change needs to take place.

Sole traders are burdened with a larger tax rate, ranging from 20-45% on profits, while also needing to allocate money for National Insurance Contributions (NIC). Limited companies pay a 20% tax on profits when the revenue generated does not exceed £300.000 and a 21% rate on £300.000<.

Elevating credibility

One important benefit of a limited company is credibility. As you begin to grow, you’ll start developing more robust relationships with your clients and suppliers. As a sole trader, the potential to expand may be stifled due to lack of credibility from your end.

Though this may not always be the case, but sole traders don’t necessarily possess the validity bigger ‘fish’ are looking for. As a limited company – that legal status imposes a sense of trust and credibility in the eyes of bigger clients or suppliers you may be looking to attract in the future.

The same thought process can be applied to potential investors. Investors who are willing to part ways with their cash may be more inclined to do so for a trustworthy limited company rather than take a gamble with a sole trader. A limited company can also raise capital by selling off a portion of its shares.

How to make the change from a sole trader to a limited company

Name

To register a limited company, you will need a company name. You may want to choose something that reflects your practice.

Bank account

The company finances need to be kept separate from your personal finances – you will need to open up a bank account in your company’s name.

Inform clients and vendors

Take some time to inform your clients and vendors of the change you’re making. They have to know that you’re operating a company – a separate legal entity. This is vital for invoicing and any future cash flow. Any checks or money transfers will have to be written out to your company.

Corporate tax

Let HMRC know that you have made the switch from a sole trader to a limited company. Fill out your self assessment tax return, and the following year you will have to submit tax returns as a director and the shareholder of the company.

You have a 3 month grace period within which you must register with the HMRC for corporate tax.

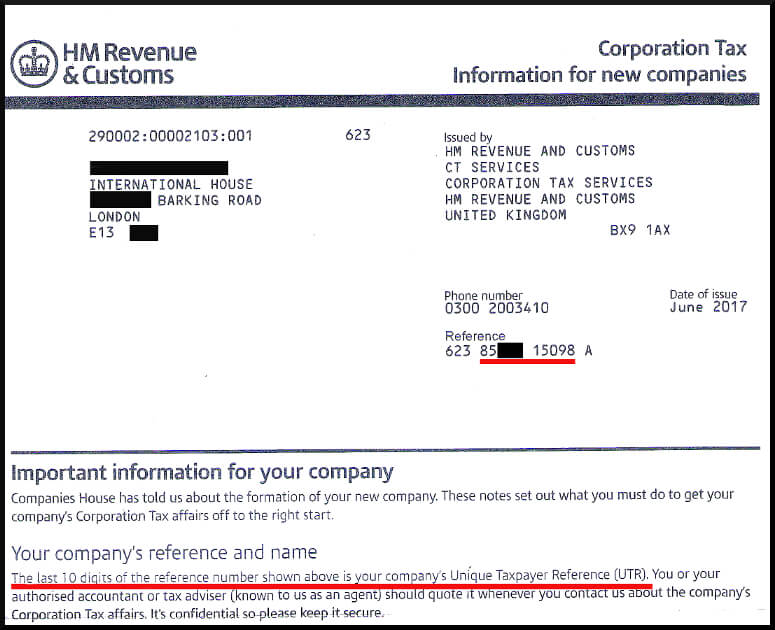

To register for corporate tax you will need –

- 10 digit Unique Taxpayers Reference (UTR);

- the date you started to do business (your company’s accounting period will start on this date);

- the date your annual accounts are made out to.

Following this, the HMRC will disclose the date by which you will have to pay your corporate tax. You will have to file a company tax return even if you have made a loss, or have no corporate tax to pay.

VAT

If you possessed a VAT number as a sole trader, you will have to cancel it. A new VAT number will have be registered by your newly created limited company within 30 days of the change.

Register as an employer

Since the company will be the one paying salary to you and your employees, it will have be registered as an employer with HMRC.

This registration must happen before the first payday. It can take up to 5 days to receive ‘pay as you earn’ (PAYE) reference number. You cannot register more than 2 months before starting to paying yourself or any other employee within the company.

To pay an employee before you receive PAYE reference number you need to –

- run payroll;

- store full payment submission;

- send a late payment submission to the HMRC.

Invoke the help of an accountant

When making the switch from a sole trader to a limited company, getting an accountant involved may be advised. Having a more competent individual participating in this process will help circumvent any potential errors and leave you with less things to worry about.

Hiring an accountant is not required though it gives you a sense of security.

That’s it!

If you have managed to get this far – congratulations, you’re now the owner of a limited company. Pay attention to the additional regulations that come with limited company operations. It may take some time to get accustomed to this new development.